Disbalance of Budget System of the Russian Federation

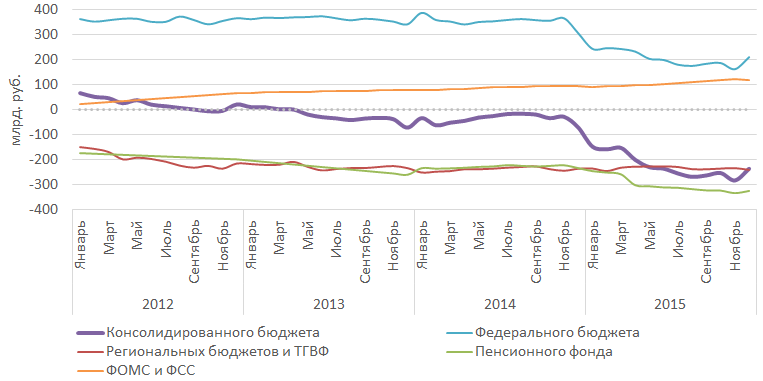

The budgetary system of the Russian Federation system is experiencing a serious deficit, budgets of the regions and the Pension Fund being the main source of the problems.

The budgetary system of the Russian Federation consists of three major levels:

- federal budget;

- regional budgets and budgets of territorial state extra-budgetary funds (hereinafter referred to as the regional budgets and TSEBF); these will be discussed together in this review;

- budgets of the state extra-budgetary funds (SEBF), comprised, in turn, of three parts – Pension Fund of the Russian Federation (PFR), Federal Compulsory Medical Insurance Fund (CMIF) and Social Insurance Fund of the Russian Federation (SIF).

hould inter-budget transfers be excluded from the budgets, it would be obvious that the regional budgets (including the budgets of the TSEBF) are consistently deficient during the past four years, and the problems in the economics have not markedly affected them; the main blow of the crisis caught directly the federal budget, and, partially, the budget of the PFR.

Inter-Budget Transfers

A lot of inter-budget transfers cannot fully compensate for their legislated expenditure obligations only at the expense of income and are obliged to rely on the help of other budgets.

The inter-budget transfers given in the table below are composed both of general purpose transfers and target transfers, which are “threaded” in the corresponding items of expenditure.

As can be seen from the table, the federal budget is a net contributor; in 2015, its net transfers to the budgets of other levels amounted to more than 4.5 trillion rubles, most of which was received by the regional budgets (jointly with the budgets of the territorial state extra-budgetary funds).

Table of inter-budget transfers for 2015 (billion rubles).

The federal budget is suffering from the drop in oil and gas incomes

One of the key reasons for the deepened deficit of the Russian budget lies in the reduced oil and gas incomes, which are in the possession of the federal budget. Drop in oil prices was not fully compensated by the devaluation of the Russian ruble, and, in consequence, in 2015 the federal budget received even lower incomes than in 2014.

Although oil and gas incomes continue to play a leading role in pumping up the federal budget, their share fell below 50% for the first time over the past five years. Incomes, related to the domestic production, increase of which has significantly accelerated since 2013, are becoming increasingly important, as well as other incomes (mainly those related to the use of state property), which showed a significant increase last year.

Growth of expenditures has slowed somewhat in comparison with the previous years, but, in contrast to the incomes, has remained positive. Strong growth of expenditures for the national economics in 2014 was almost entirely concentrated in this December (over 1.5 trillion rubles) and was been associated with the devaluation of the ruble. In absolute terms, the highest growth was demonstrated by the expenditures for the national defense: their growth rates increased during last year.

The federal budget spends most of the funds to support other levels of the budget, and should these transfers be excluded from the incomes and expenditures, the federal budget would still a surplus budget, even despite the drop in the oil and gas incomes.

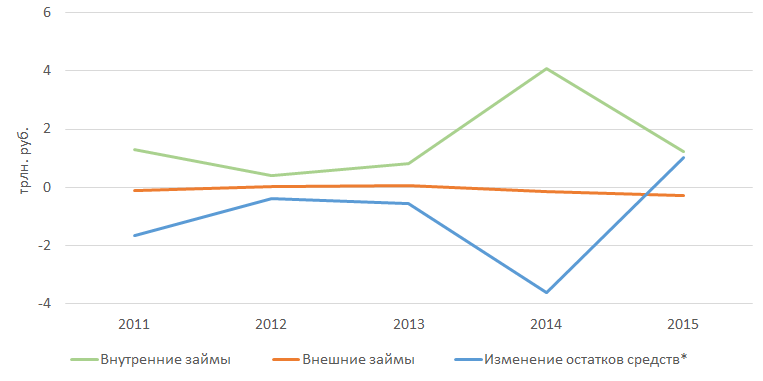

Domestic market borrowings are the main source of financing of the federal budget deficit. In 2014, the budget borrowed about 4 billion rubles, but spent these funds only in 2015.

Incomes of the federal budget federal budget

* Incomes from the use of property, from the provision of paid services, from state duties, etc.

Expenditures of the

* National security and law enforcement activities

** Housing and utilities infrastructure, environment protection, physical training and sports, mass media

Sources of financing of the federal budget

* (+) decrease in the balance, (-) increase in the balance

Incomes, expenditures and sources of financing of the federal budget

* (+) decrease in the balance, (-) increase in the balance

Budgets of the regions of the Russian Federation Depend on Transfers

The situation with respect to the regional budgets, including the budgets of the territorial state extra-budgetary funds, remains so far relatively stable. Profit tax and transfers from other budgets (of course, from the federal budget, in the first place) still remain the key sources of financing, and their breakaway from other sources keeps growing at priority growth rates.

The expenditures do not show any particular growth tendency almost everywhere, except for public health services only; over the past year, stagnation has even been observed in nominal terms, but in terms of inflation, all the expenditures (except for public health services) have decreased since 2014. A particularly strong failure is observed in the expenditures for the housing and utilities infrastructure – the average slowdown in these expenditures has amounted to 3% since 2011.

However, without transfers, the regional budgets are consistently deficient (the deficit amounted to 2.8 billion rubles in 2015), and, recently, albeit slowly, but the situation, has been worsening.

The regional budgets practically do not use external market borrowings to finance the budget deficit, using, predominantly, Russian bond market borrowings.

Sources of financing of regional budgets and TSEBF

** Incomes from the use of property, from the sake of assets, etc.

*** (+)decrease in the balance, (-) increase in the balance

Expenditures of regional budgets and TSEBF

Pension Fund

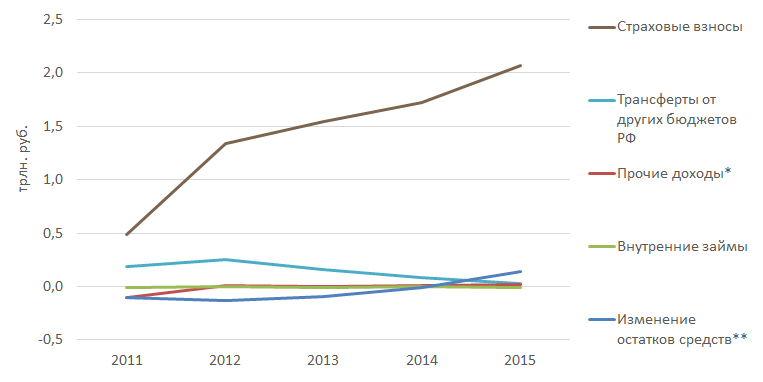

The sources of financing of the Pension Fund of the Russian Federation are composed of the two components – insurance contributions and transfers of other budgets (from the federal budget, in the first place). After the failure in 2014 (when the transfers amounted to 66% of the insurance contributions), the inter-budget non-repayable assignments returned to the previous level (about 85% of the insurance contributions). Without help from other budgets, the PFR would have felt a deficit of 2.3 billion rubles in 2015.

In addition, the PFR starts financing its deficit independently, and with higher activity, increasing the domestic market borrowings.

Sources of financing of the Pension Fund

* Incomes from the use of property, provision of paid services, etc.

** (+) decrease in the balance, (-) increase in the balance

Federal Compulsory Medical Insurance Fund and Social Insurance Fund of the Russian Federation

The situation with respect to the two other state extra-budgetary funds (CMIF and SIF, their incomes and expenses being much lesser, about 30% of the PFR) is somewhat different – inter-budget transfers have never played a significant role in their incomes, especially in the recent years, with the transfers steadily tending to zero. Thus, the insurance contributions fully cover the expenditure obligations of these funds, which are already almost independent of inter-budgetary transfusions, with their remaining consistently surplus budgets over the past years.

Sources of financing of the CMIF and SIF

* Incomes from the use of property, etc.

** (+) decrease in the balance, (-) increase in the balance

The Way the Budget Deficit Could Be Financed

The Government of the Russian Federation has two main sources to cover the budget deficit: firstly, these are the reserves and, secondly, the borrowings (both domestic and foreign market borrowings).

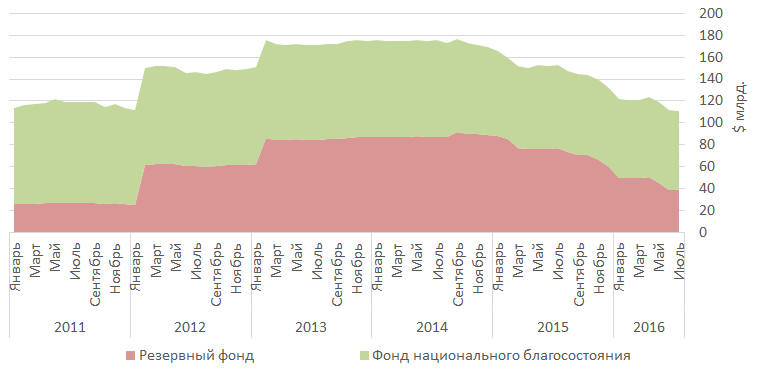

The reserves to cover the federal budget deficit (through the transfers from which deficits of other budgets will also be eliminated) are stored in the Reserve Fund. If the funds of the Reserve Fund are spent at the rates they were spent over the past eighteen months, it will be completely depleted by September 2017, that is, within a year, the government will have to use the second option.

As has already been mentioned above (see the review named External Debt of Russian Economics) with the current income yield of Russian government bonds, the government may borrow another $ 73 billion (or 4.7 billion at the current rate of exchange) on the foreign market, thus coming up with the USA in debt-management costs. Under the condition of stagnation of the Russian economics and preservation of the consolidated budget deficit at the level of 4% of the GDP, the funds to be received will be sufficient for almost two years.

There is one more source, which will help to stabilize the budget for a while, and this is privatization. The government planned to sell 19.5% of Rosneft and 50.1% of Bashneft, which, with their current capitalization, will amount to approximately 1 trillion rubles. Most probably, privatization of these two assets will take place in 2017.

Thus, the Reserve Fund, foreign credits and privatization of share packages of Rosneft and Bashneft may finance the budget deficit for another three and a half years, which (it is hoped) will be used by the government for large-scale structural reformation of the domestic economics.

Reserves of the Russian Government

To cover the budget deficit, the Government of the Russian Federation has the Reserve Fund, the main task of which is precisely to enforce execution of the expenditure obligations by the state in case of reduced oil and gas incomes. The current situation satisfies these conditions in full, and since the start of 2015, the Reserve Fund has been gradually depleted, covering the budget deficit.

The National Wealth Fund (hereinafter referred to as the NWF) has different tasks to be solved – it is called to cover directly the deficit of the Pension Fund of the Russian Federation. However, as has already been mentioned above, a considerable part of incomes of the PFR is comprised of the transfers from the federal budget. In case of depletion of the Reserve Fund, the NWF may become a major donor of the PFR, which, correspondingly, will reduce the expenditures of the federal budget, which will get rid of the need to direct substantial funds for transfers for the Pension Fund. Thus, the NWF may reduce the federal budget deficit, without deviating from its official mission.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}